Since A Picture Is Worth A Thousand Words, We’ll Be Brief

Published Wednesday, July 20, 2022 at: 9:23 PM EDT

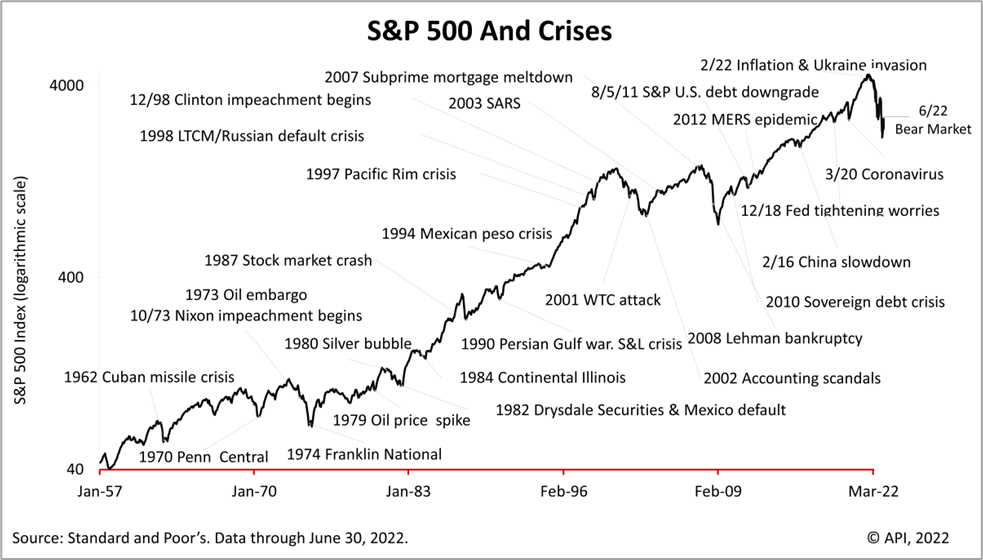

By our count, the bear market of 2022 is the latest of more than 20 market crises that came and went since 1957.

The bear market of 2022 began June 13, when the Standard & Poor’s 500 index closed more than -20% lower than its all-time closing high on January 3, 2022.

No one knows how long the bear market will last. The average bear market in modern history lasts about 11 months. On the other hand, having come off its low of June 16, this bear market might be over already. Strong economic fundamentals belie fears of a sharp downturn.

Amid recent uncertainty, remember that the U.S. stock market rose despite the onslaught of crises that have plagued modern history.

Is the inflation crisis of 2022, which comes on the heels of the Ukraine crisis, somehow how different from the Cuban missile crisis, 9/11, or the pandemic?

Selling stocks in a crisis is very likely to result in missing the recovery. While recent events are testing investor resolve, history indicates that the best strategy for building wealth is to stay put for the long run, even if it’s hard to do.

Nothing contained herein is to be considered a solicitation, research material, an investment recommendation, or advice of any kind, and it is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Tax advice always depends on your particular personal situation and preferences. You should consult the appropriate financial professional regarding your specific circumstances. The material represents an assessment of financial, economic and tax law at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions. This article was written by a professional financial journalist for Advisor Products and is not intended as legal or investment advice.

This article was written by a professional financial journalist for Preferred NY Financial Group,LLC and is not intended as legal or investment advice.

An individual retirement account (IRA) allows individuals to direct pretax incom, up to specific annual limits, toward retirements that can grow tax-deferred (no capital gains or dividend income is taxed). Individual taxpayers are allowed to contribute 100% of compensation up to a specified maximum dollar amount to their Tranditional IRA. Contributions to the Tranditional IRA may be tax-deductible depending on the taxpayer's income, tax-filling status and other factors. Taxed must be paid upon withdrawal of any deducted contributions plus earnings and on the earnings from your non-deducted contributions. Prior to age 59%, distributions may be taken for certain reasons without incurring a 10 percent penalty on earnings. None of the information in this document should be considered tax or legal advice. Please consult with your legal or tax advisor for more information concerning your individual situation.

Contributions to a Roth IRA are not tax deductible and these is no mandatory distribution age. All earnings and principal are tax free if rules and regulations are followed. Eligibility for a Roth account depends on income. Principal contributions can be withdrawn any time without penalty (subject to some minimal conditions).

©2022 Advisor Products Inc. All Rights Reserved.